Southeast Asia’s private equity market remained subdued in 2025, with total deal value declining about 10 percent year-on-year to $14.3 billion across 84 transactions, according to the “Southeast Asia Private Equity Report 2026” report conducted by Bain & Company.

In a release on Friday, Bain & Company said the recovery across the region has been uneven, with capital concentrated in a limited number of large transactions, reflecting broader trends in the Asia-Pacific market. Singapore took the lead with $7 billion in 2025, down from $7.4 billion in 2024.

Despite the region’s downtrend, Malaysia bucked the trend with $5.3 billion last year, up from $1.9 billion in 2024.

Deal activity was driven primarily by growth and buyout investments. Government-linked investors played a larger role in high-value transactions, frequently partnering with global and regional funds. A small number of large deals accounted for a disproportionate share of overall value.

While capital remains available, investment activity has become more selective. Investors are prioritizing assets with strong management, clear competitive positioning, and defined exit strategies, amid a limited pool of high-quality opportunities.

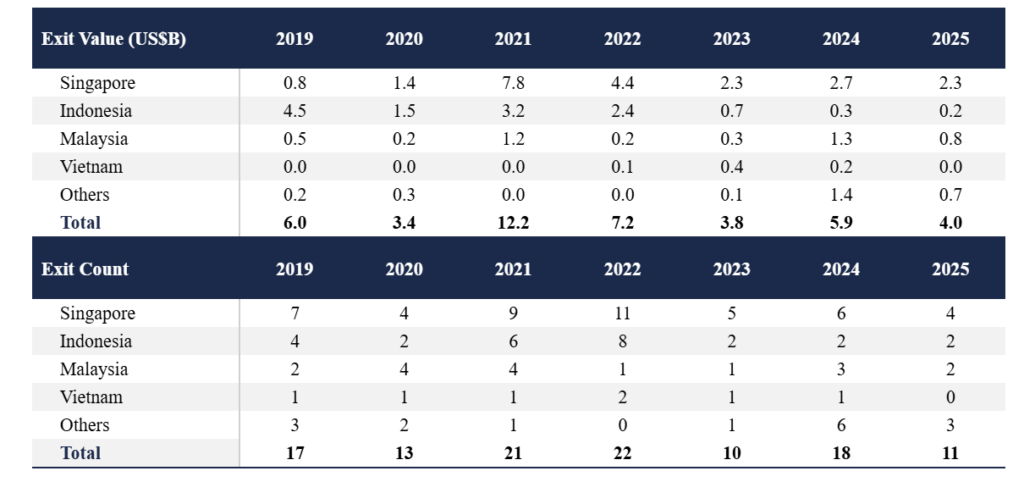

Exit activity continues to weigh on the market. Exit value fell by 32 percent in 2025 to $4 billion, with trade sales remaining the primary exit route. Initial public offerings showed early signs of recovery, but overall exit volumes remained constrained. Longer holding periods have led to an increase in aging assets, with secondary transactions becoming a more prominent route to liquidity.

Tom Kidd, head of Southeast Asia Private Equity at Bain & Company, said the market is stabilizing but remains shaped by exit challenges. He noted that capital is increasingly concentrated in fewer deals, with investors taking a more selective approach.

As exit timelines extend, firms are placing greater emphasis on operational improvements to drive returns. Value creation strategies are increasingly focused on EBITDA growth through cost management, pricing strategies, and commercial performance, rather than relying on multiple expansion. Artificial intelligence (AI) is also becoming more integrated into investment processes, with more than 70 percent of investors reporting its use, primarily for productivity improvements.

Sector investment trends reflect structural growth themes. Digital infrastructure and AI-related technologies, including data centers, are attracting strong interest. Healthcare has seen deal value increase by around 60 percent over the past five years, driven by consolidation and platform development. Manufacturing and industrial sectors are benefiting from supply chain diversification, particularly in Vietnam and Indonesia. In financial services, fintech remains an area of focus, while consumer investments are shifting toward localized and value-oriented offerings.

Singapore remained the region’s leading hub for dealmaking, accounting for the largest share at $7 billion. Malaysia recorded the strongest year-on-year growth in deal value, reaching $5.3 billion. Exit activity, however, stayed limited, with Singapore reporting four exits and Vietnam recording none.

A survey of private equity investors across Asia-Pacific indicates continued caution toward Southeast Asia. Key concerns include exit challenges, fundraising pressures, and limited availability of high-quality deals. Many investors expect returns to depend more on revenue growth and operational improvements, with reduced reliance on leverage.

Across the broader Asia-Pacific region, exit activity is beginning to recover and improve liquidity, though fundraising remains under pressure and macroeconomic uncertainty continues.

Southeast Asia private equity stalls to $14B in volatile 2025