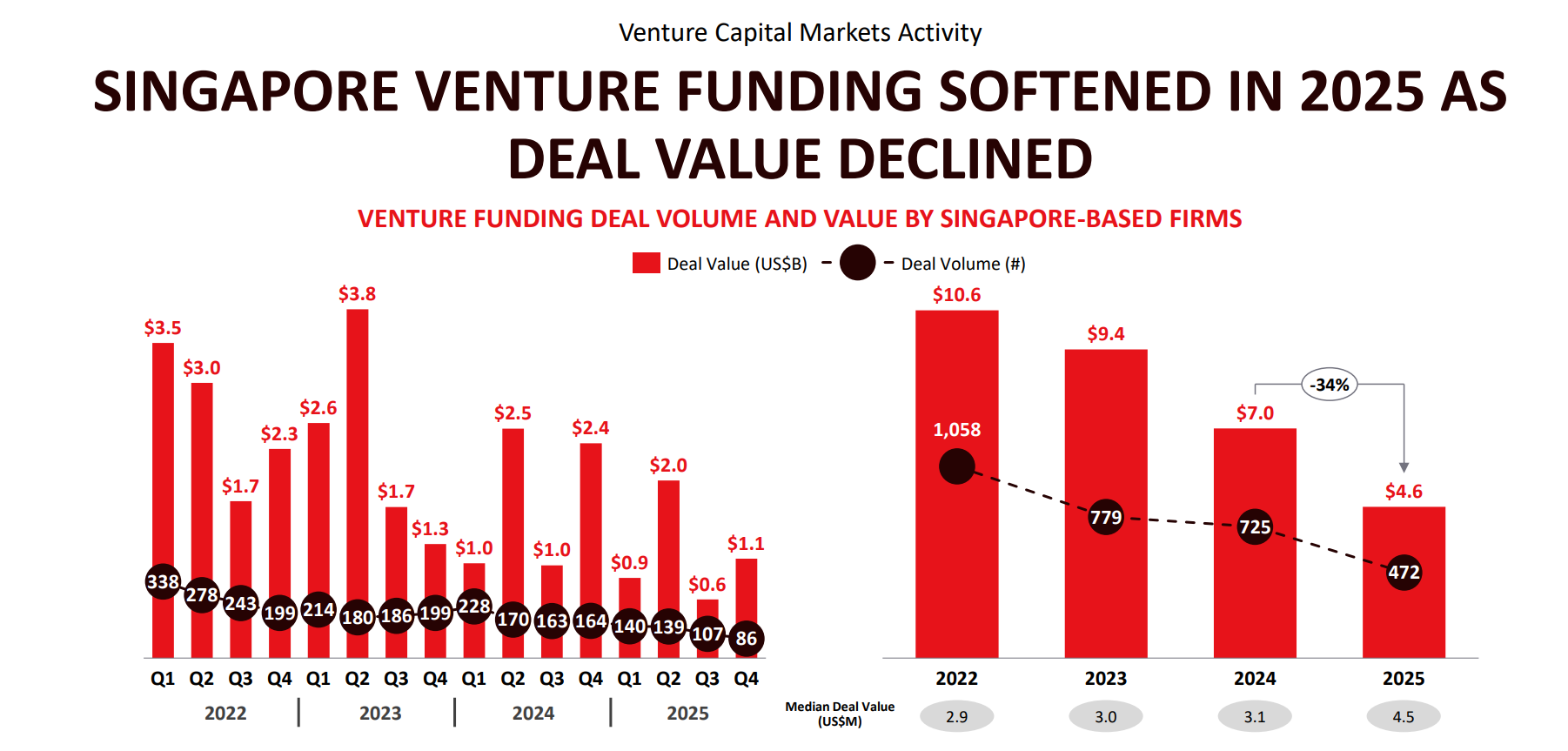

Singapore’s venture capital market contracted sharply in 2025, recording 472 deals worth a combined $4.6 billion, a 35 percent decline in deal volume and a 34 percent drop in deal value compared to the year prior, according to the Singapore Venture Funding Landscape 2025 released on Thursday.

The report, compiled by EY Parthenon, showed that the numbers mark the third consecutive year of cooling since the pandemic-era peak of $10.6 billion across 1,058 deals in 2022, as higher interest rates, muted exit markets, and a more disciplined investor class reshaped the city-state’s startup ecosystem.

Fewer Deals, Greater Scrutiny

The drop in deal count reflects a deliberate shift in how investors are deploying capital. Investors are now placing far greater emphasis on due diligence and clear pathways to profitability before committing funds. Speculative bets on unproven growth narratives have fallen out of favor, replaced by a preference for startups with growth narratives.

Late-stage deals accounted for 33.3 percent of total deal volume in 2025, up from 26.9 percent in 2024. Meanwhile, early-stage activity contracted, as investors grew more cautious.

The median deal value, however, rose to $4.5 million in 2025, up from $3.1 million in 2024.

4 Industries Drive the Market

Despite the broader slowdown, four industries dominated Singapore’s venture landscape in 2025, accounting for 69 percent of total deal volume and 82 percent of total deal value.

Fintech retained its position as Singapore’s largest funded sector, with deal value rising 34 percent year-on-year to $1.7 billion, bucking the overall downward trend. The growth was driven primarily by financial software and reinforced by Singapore’s structural role as ASEAN’s financial hub. A deep ecosystem of over 1,500 fintech firms, global financial institutions, and a supportive regulatory environment from the Monetary Authority of Singapore helped attract growth-stage capital.

The concentration at the top was stark astwo Airwallex fundraising rounds totaling $631 million, alongside Bolttech’s $147 million raise, accounted for more than 45 percent of total fintech deal value.

Enterprise software and data infrastructure saw deal value compress sharply from $2.2 billion to $1.0 billion, or a 53 percent decline. Traditional software-as-a-service (SaaS) models, long underpinned by seat-based licensing and switching costs, are facing a structural challenge from generative AI. As AI agents compress application layers, legacy moats are weakening, and capital is being repriced accordingly. The money is not leaving the category but it is repositioning toward enabling AI infrastructure, developer tooling, and vertically integrated AI platforms.

Healthcare and biomedical raised $584 million across 42 deals. Notable transactions included Callio Therapeutics, which closed a $187 million Series A to advance its antibody-drug conjugate cancer platform, and Nuevocor, which raised $45 million for first-in-human clinical trials of a cardiomyopathy gene therapy across the United States and Europe.

Advanced manufacturing attracted $466 million across 37 deals, with investment anchored in robotics, industrial automation, and semiconductors — areas increasingly relevant to global demand for AI-ready infrastructure. —

Artificial Intelligence: The Cross-Cutting Investment Theme

Artificial intelligence (AI) has emerged not as a single sector but as a transformative lens through which capital is being redeployed across all industries. In 2025, AI-related deal value grew from $1.1 billion to $1.4 billion, even as overall venture activity declined. AI’s share of total deal value doubled to 31 percent, and its share of deal volume rose to nearly 43 percent. The figure indicated strong investor conviction and capital concentration into AI-led opportunities.

The AI investment story in Singapore is inseparable from the country’s policy architecture. Singapore established its first National AI Strategy in 2019 and launched the world’s first Model AI Governance framework. NAIS 2.0, launched in 2023, sharpened focus on both frontier AI development and broad-based enterprise adoption. The country now ranks 7th on the 2025 Oxford Insights Government AI Index and hosts more than 1,000 AI startups, over 150 research and product teams, and more than 80 AI research faculty.

From 2026 to 2030, Singapore has committed S$37 billion ($28.9 billion) in national research and innovation funding, including S$1 billion specifically earmarked for public AI research, the report showed. AI missions are slated to launch across four priority sectors of finance, connectivity, advanced manufacturing, and healthcare in 2026.—

Southeast Asia in a Downturn

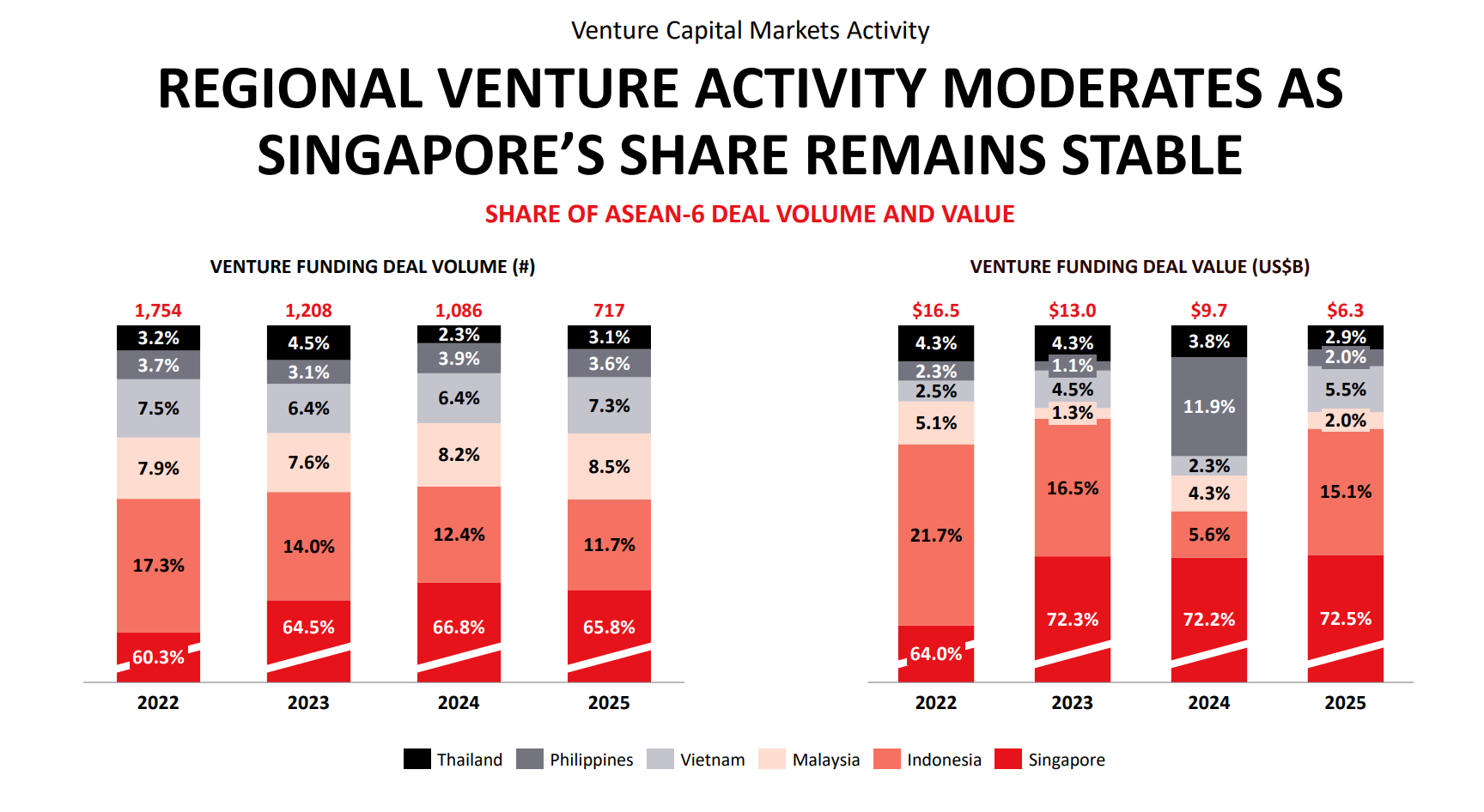

Singapore’s difficulties are similar to a broader regional correction. Across the ASEAN-6 (Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam), total deal value fell to $6.3 billion in 2025 from $9.7 billion in 2024, with deal volumes declining to 717 from 1,086. Both metrics represent four-year lows.

The region’s slowdown reflects global capital recalibration. Major sources of venture funding from the United States and China have grown more focused on domestic priorities, reducing cross-border flows, according to Remi Choong, Principal at Elev8.vc.

Nevertheless, Singapore has maintained its dominant position within the region. The city-state commanded a 72.5 percent share of ASEAN-6 venture deal value in 2025, r.

Singapore-based East Ventures pushes emissions cut, expands sustainability across Southeast Asia