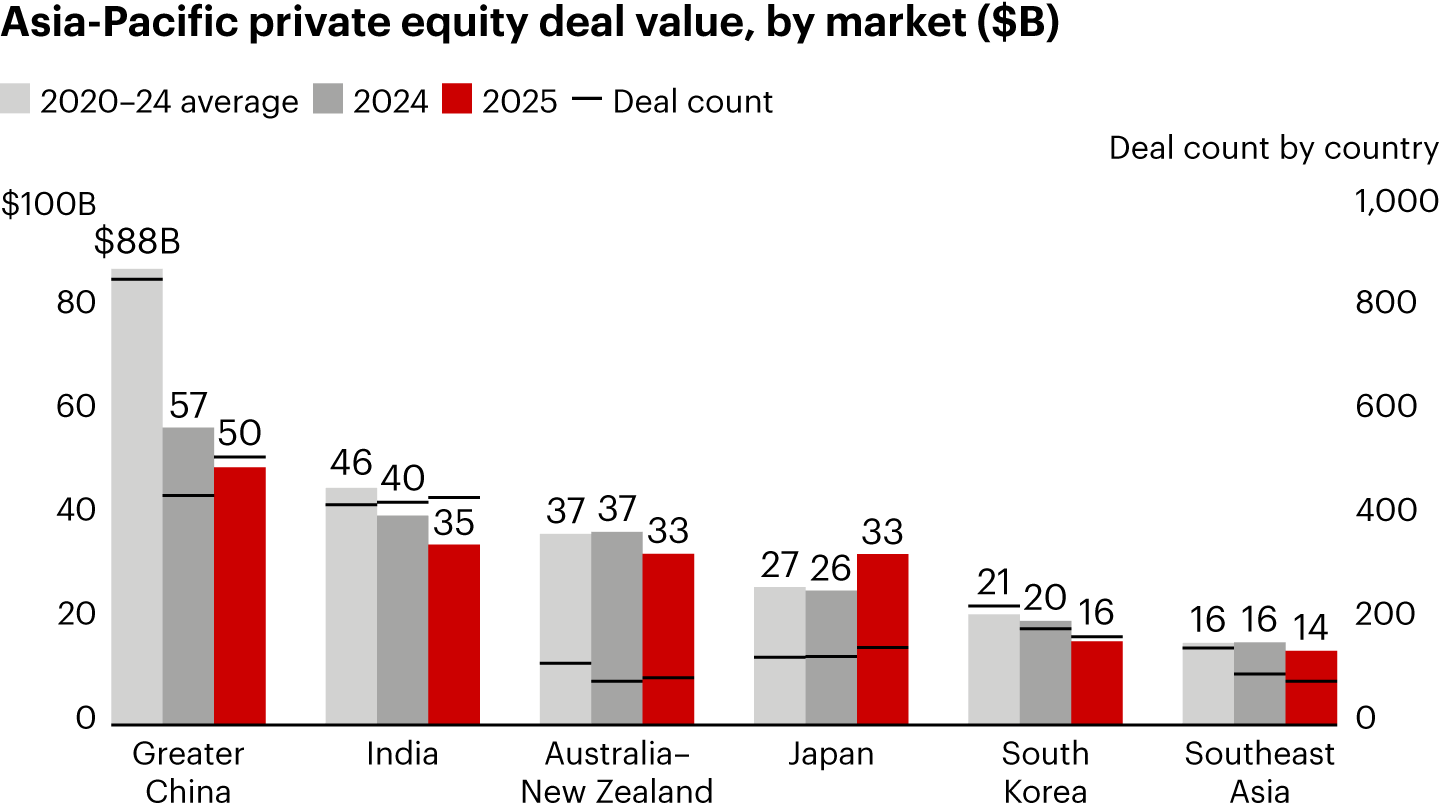

Private equity activity in Southeast Asia slowed to $14 billion in 2025, reflecting a broader pattern of volatility across the Asia-Pacific region, as investors grappled with global trade tensions, elevated valuations, and persistent fundraising challenges.

According to a new report released by Bain & Company on Tuesday, deal value in Southeast Asia declined from $16 billion in 2024 and the average figure of $16 billion in 2020-2024. The region’s exposure to global trade dynamics made it more vulnerable for sectors tied to export activities due to tariff uncertainty. It also contributed to softer investment activity even as overall deal count across Asia-Pacific rose modestly.

Source: Bain & Company’s Asia-Pacific Private Equity Report 2026

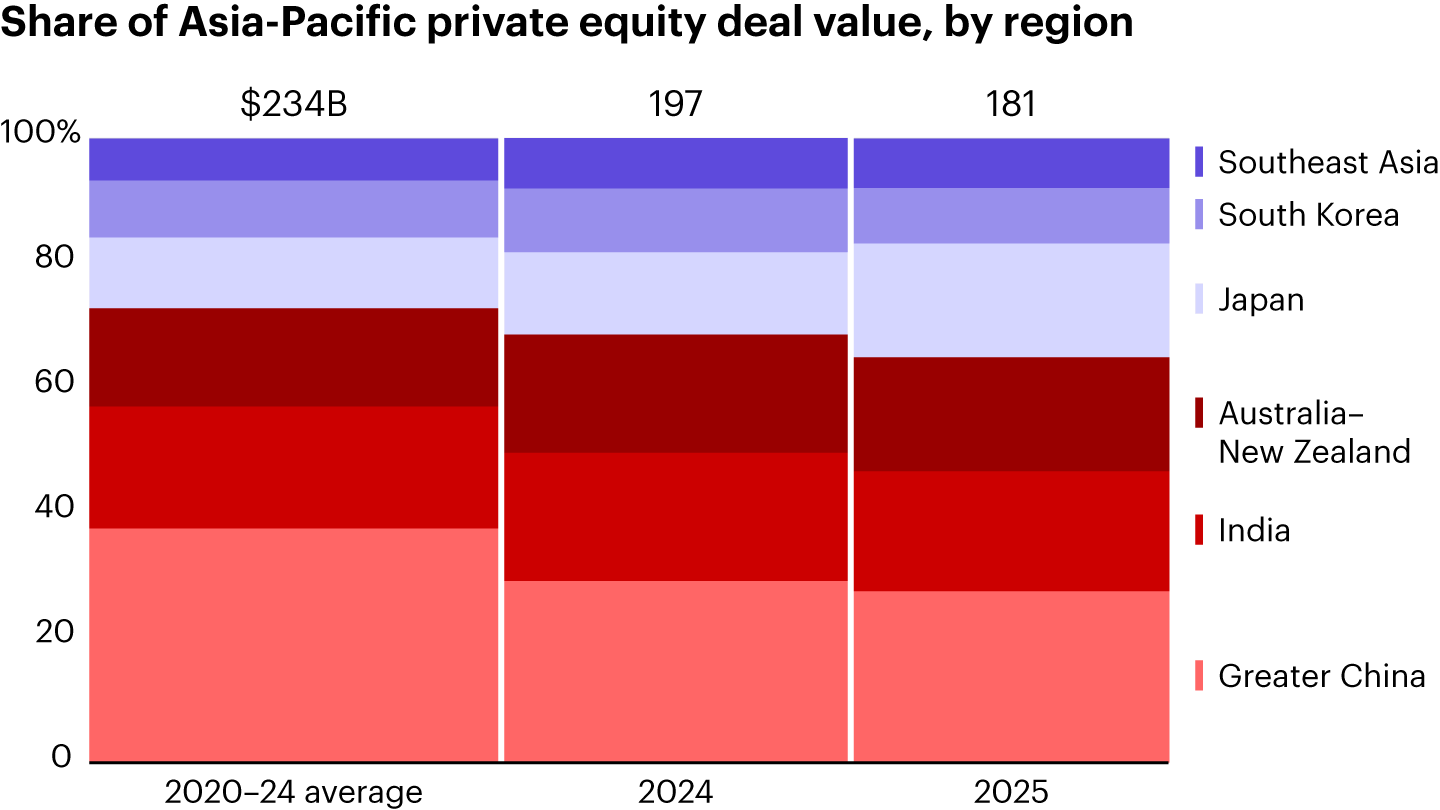

Regarding total deal value, Southeast Asia accounted for less than 10 percent, also the smallest portion in Asia-Pacific. The broader region recorded a total figure of $181 billion, with China, India, and Australia-New Zealand accounted for the biggest figures. Others key markets were Japan and South Korea.

Source: Bain & Company’s Asia-Pacific Private Equity Report 2026

Similar to Southeast Asia, Asia-Pacific deal value dropped 8 percent year on year, even as deal count rose 6 percent, highlighting a cautious but still active investment environment.

Quarterly performance underscored the instability. Deal value surged more than 20 percent in the first quarter, plunged to its lowest level since 2020 in the second quarter following tariff shocks, rebounded 15 percent in the third quarter, and then fell more than 10 percent in the fourth quarter.

Technology, media, and telecommunications remained the largest sector but fell to 25 percent of total deal value, a 10-year low. Retail emerged as a growing focus, reaching 9.2 percent of total deal value, supported by post-pandemic recovery and government measures to boost domestic consumption.

Buyouts continued to dominate, accounting for roughly 50 percent of total deal value, though the average buyout size dropped to $438 million, down from $630 million in 2024. The number of mega-buyouts (over $1 billion) declined to 22 deals, while fewer transactions exceeded $10 billion. At the same time, valuations rose, with median deal multiples increasing to 13.4x EBITDA, up from 11.9x a year earlier.

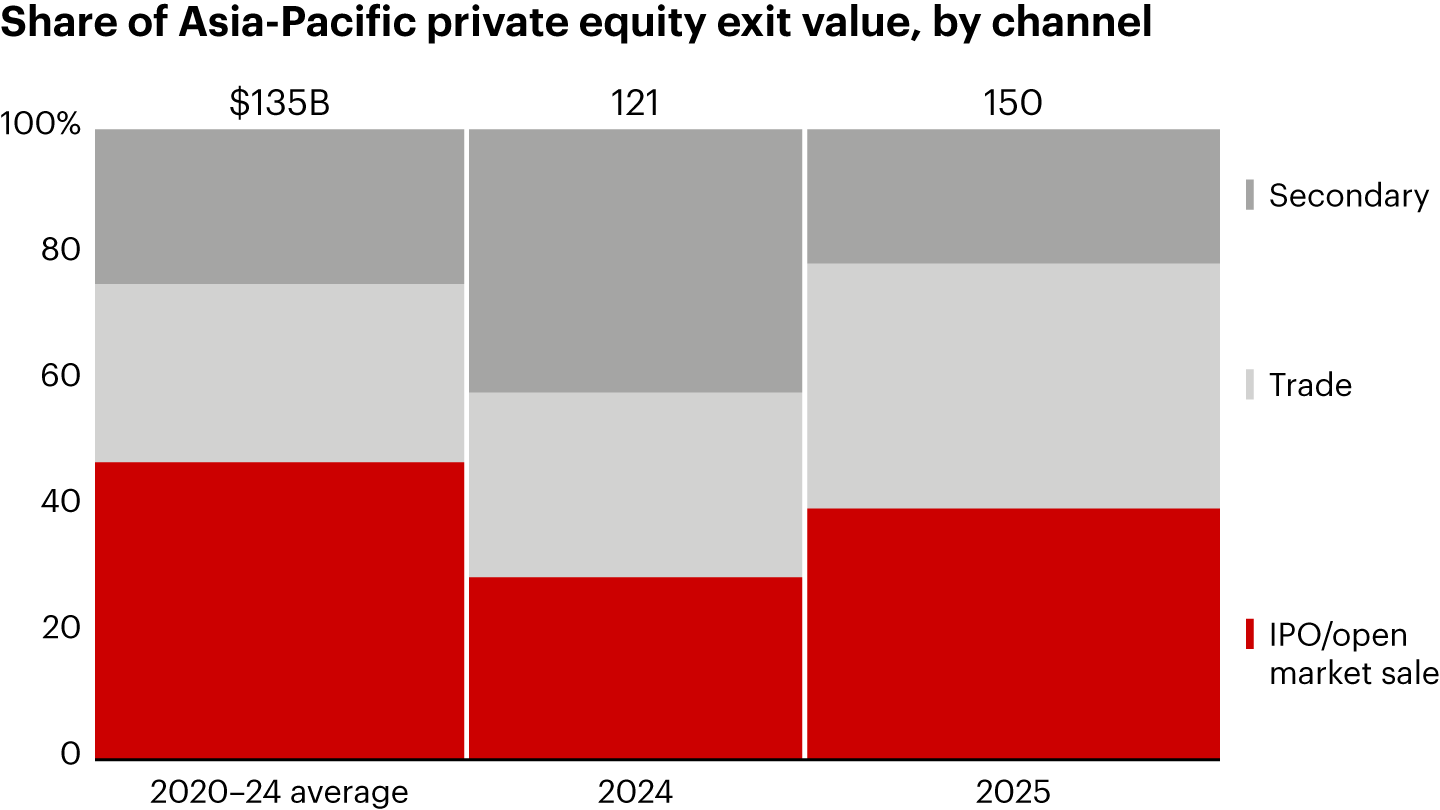

Exits rise 24 percent, but Southeast Asia remains subdued

Exit markets provided a key bright spot. Across Asia-Pacific, exit value rose 24 percent from $121 billion in 2024 to $150 billion in 2025, while exit count increased 8 percent, marking the second consecutive year of recovery. However, Southeast Asia’s exit count remained muted, as tariff uncertainty continued to dampen demand for export-driven assets.

Trade sales also remained robust, growing more than 60 percent, with major transactions across the region including: Singapore-headquartered Temasek’s $6.4 billion sale of Schneider Electric India, Bain Capital’s $4.0 billion sale of WinTriX DC Group in Greater China, Macquarie’s $3.3 billion sale of DIG Airgas in South Korea, KKR’s $2.6 billion sale of Seiyu in Japan, and Brookfield’s $2.5 billion sale of Aveo in Australia–New Zealand.

Still, structural pressures remain. The number of portfolio companies held for more than five years rose 18 percent, while average holding periods increased from 3.7 years to 4.0 years, reflecting a growing backlog of aging assets.

Fundraising across Asia-Pacific fell 37 percent year-on-year to $58 billion, the lowest level in over a decade, while fund count dropped 44 percent. The six largest funds launched in 2025 are targeting a combined $61 billion. These include KKR Asian Fund V ($15 billion target), EQT’s BPEA Fund IX ($12.5 billion), Blackstone Asia Fund III ($10 billion), KKR Asia Pacific Infrastructure Investors III ($9 billion), Bain Capital Asia Fund VI ($7 billion), and Hillhouse’s latest Asia private equity fund ($7 billion). By the end of 2025, these funds had disclosed approximately $25 billion in secured commitments.

Asia-Pacific is re-emerging as a priority region for global limited partners – Coller Capital